ZET App Review – if you’re searching this, you’re probably someone who wants a credit card but keeps hitting the same wall: no credit history means no card, and no card means no credit history. It’s a frustrating loop that millions of salaried and self-employed Indians face every year.

I’ve been there. And after testing ZET personally, I can tell you it solves this specific problem better than most alternatives currently available in India.

This ZET App review covers everything – what it is, how it works, the FD requirement, interest earned, fees, credit score impact, safety, RBI approval status, and who should and shouldn’t use it.

By the end, you’ll know exactly whether ZET is the right tool for your financial situation.

👉 If you’ve already decided to try it: Download ZET using my referral link

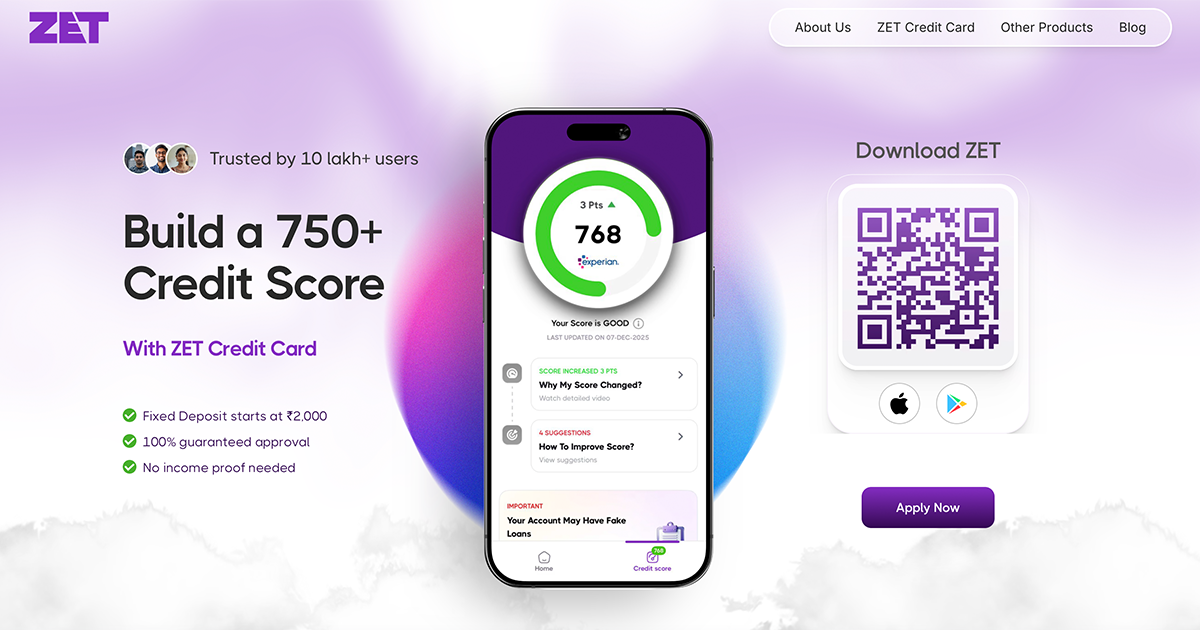

What Is ZET?

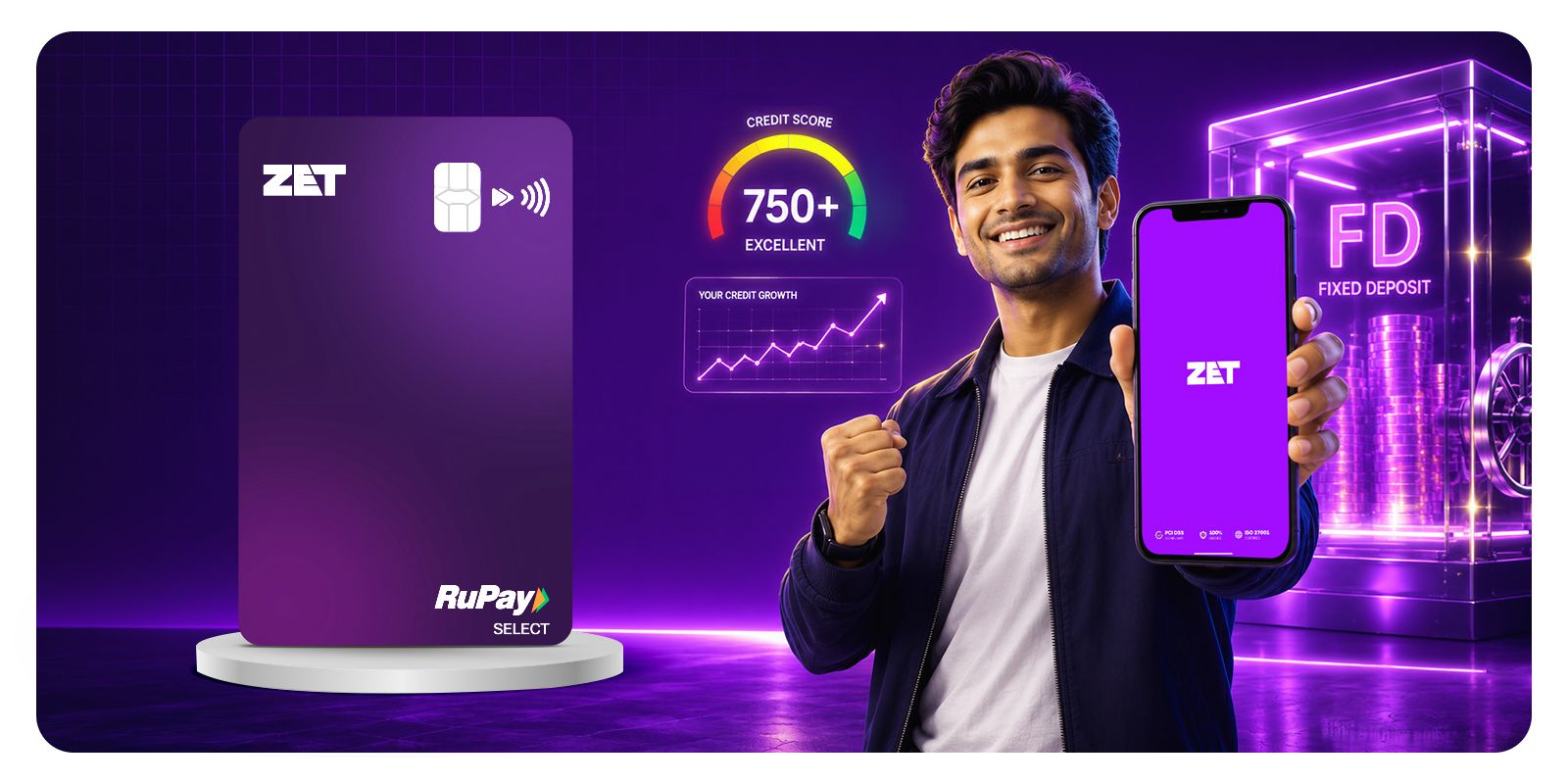

ZET is a fintech app that offers a secured credit card backed by a Fixed Deposit (FD). The concept is simple: you deposit a minimum amount as an FD, and ZET issues you a credit card against that FD. Your deposit stays yours – it earns interest – and the credit card helps you build a credit history with bureaus like CIBIL and Experian.

ZET Full Form: ZET does not officially stand for a specific acronym – it is the brand name of the product. The company behind it is a registered fintech entity operating in India’s digital lending and credit space.

The app is designed specifically for:

- People with zero credit history

- First-time credit card applicants who get rejected elsewhere

- Young professionals, students, and gig workers building credit from scratch

- Anyone who wants a credit card without income proof dependency

The ZET Credit Card is a lifetime free secured credit card – meaning no annual fee, no joining fee. You fund it with your own FD, use it like a regular credit card, and the on-time payment activity gets reported to credit bureaus – gradually building your credit score.

How Does ZET Work?

The ZET model is straightforward and worth understanding clearly before signing up.

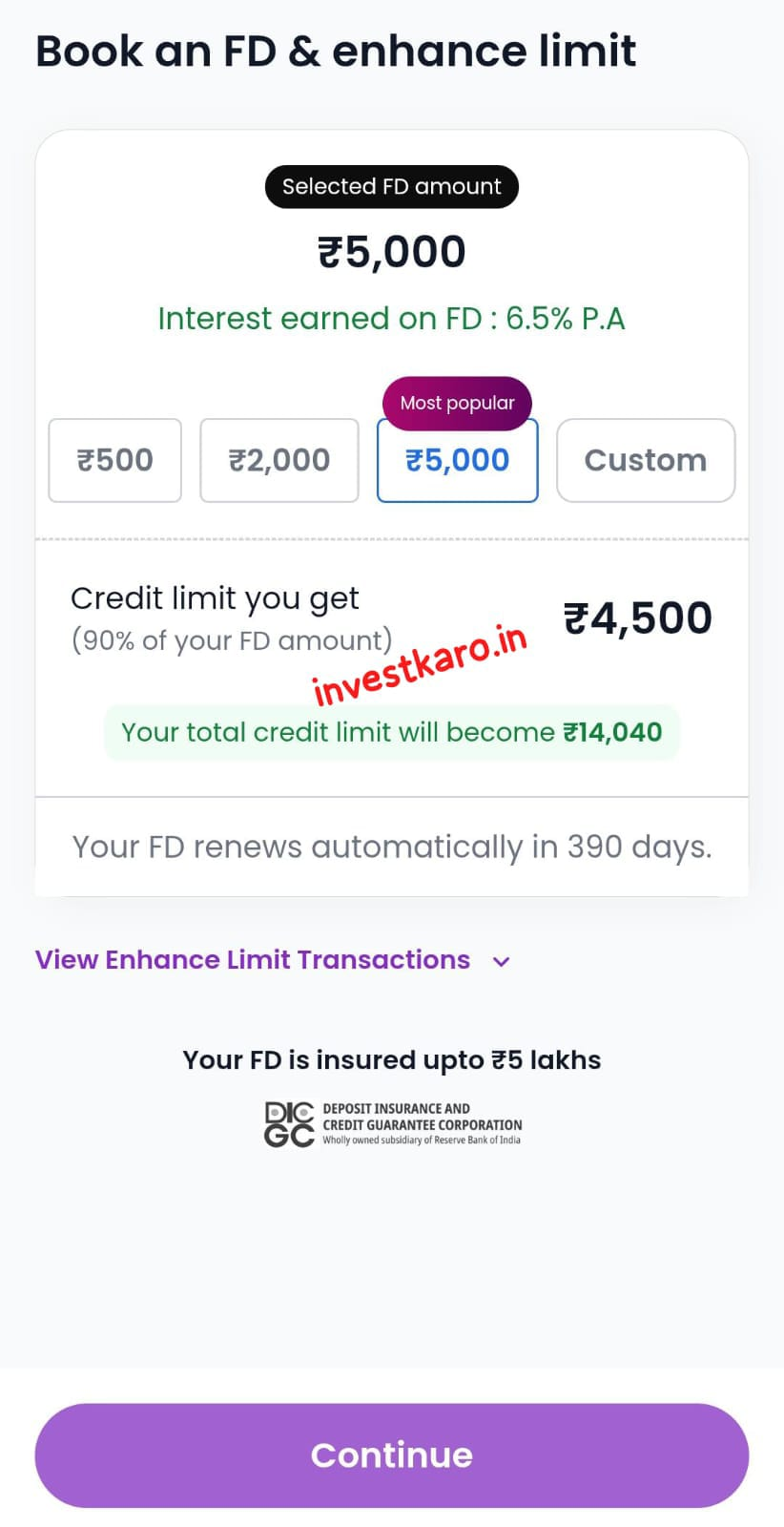

Step 1: Create your FD You deposit a minimum of ₹2,000 as a Fixed Deposit through the ZET app. This FD is your own money — it is not consumed by ZET. It sits in your account earning interest.

Step 2: Get your secured credit card Based on your FD amount, ZET issues you a credit card with a credit limit typically set at 100% of your FD value. Deposit ₹5,000, get a ₹5,000 credit limit. Deposit ₹20,000, get a ₹20,000 credit limit.

Step 3: Use the card for regular purchases The ZET Credit Card works like any standard credit card — online purchases, utility bills, subscriptions, offline payments where cards are accepted.

Step 4: Pay your bill on time every month This is the critical step. Every on-time payment is reported to CIBIL and Experian. Over 6–12 months of responsible usage, your credit score begins to build. Most users with no prior credit history start seeing a CIBIL score emerge within 3–6 months of consistent usage.

Step 5: Credit score unlocks mainstream financial products Once you have an established credit score of 700+, you become eligible for unsecured credit cards, personal loans, home loans at better rates — the mainstream financial products that were previously unavailable due to thin credit file.

Important Note: ZET’s credit-building impact depends entirely on your payment behaviour. Late or missed payments will negatively affect your score, just as they would with any credit card. Use it responsibly.

ZET Full Form and Background

ZET is a digital-first fintech platform targeting India’s large underbanked and credit-invisible population — the estimated 400+ million Indians who have no credit score and therefore no access to formal credit products.

The platform operates as a technology layer connecting users to regulated banking and NBFC partners for the underlying FD and credit card products. This is a common and legitimate structure in Indian fintech — similar to how platforms like Slice, OneCard, and Uni work with partner banks.

Key Features of ZET App

FD-Backed Secured Credit Card

The core product of ZET is the secured credit card. Unlike unsecured credit cards that require income proof, salary slips, and a minimum CIBIL score, the ZET Credit Card requires only your FD as security. No income document. No credit score requirement. No employment verification.

Credit Score Building — Reported to CIBIL and Experian

Every transaction and payment on your ZET Credit Card is reported to major credit bureaus. This is the foundational purpose of the product. For users with zero credit history, consistent use of the ZET card creates a credit trail that bureaus can score — turning an invisible credit profile into a visible, scoreable one.

Minimum FD of ₹2,000

The barrier to entry is intentionally low. At ₹2,000 minimum FD, ZET is accessible to students, gig workers, and entry-level salaried individuals who cannot commit thousands of rupees to a bank FD just to get a secured card. Most competing secured card products require ₹5,000–₹25,000 minimum FD.

Earn Interest on Your FD

Your deposited amount earns interest — up to 7% per annum at the time of writing (rates are subject to change and should be verified in the app at time of sign-up). This is a meaningful differentiator: you are not just locking your money away unproductively. The FD generates passive income while simultaneously powering your credit card.

Lifetime Free Card

The ZET Credit Card carries no joining fee and no annual fee — it is a lifetime free card. For a secured credit card targeting users with no credit history, eliminating the annual fee removes a meaningful cost burden from people who are already in the early stages of their financial journey.

Instant Activation

The ZET onboarding process is fully digital and fast. KYC is completed via the app, FD is created digitally, and the credit card is activated almost instantly for online use. The physical card follows by courier.

Credit Score Tracking

The ZET app includes a built-in credit score monitoring feature. You can track your CIBIL score progress over time — seeing the tangible result of your responsible card usage month by month. This visibility is motivating and helps users stay on track.

ZET Credit Card Review: The Honest Assessment

The ZET Credit Card is a secured credit card, which means it functions as a credit-building tool more than a rewards or cashback product. Let me be direct about what it is and what it isn’t.

What it is:

- A legitimate credit card that helps you build credit history

- A product accessible to people rejected by mainstream banks

- A sensible first credit card for someone starting from zero

What it isn’t:

- A rewards-heavy card with cashback or travel points

- A high-limit card for large purchases

- A replacement for an established premium credit card

The ZET Credit Card review picture is positive for its intended use case — credit building — and honest about its limitations. If you’re looking for airport lounge access and dining rewards, this is not your card. If you’re looking to establish a credit profile and unlock future financial products, this is exactly the right card.

ZET Credit Card Minimum FD Amount

The minimum FD required to get the ZET Credit Card is ₹2,000.

This is one of the lowest minimums among secured credit card products in India. For comparison:

| Product | Minimum FD Required |

|---|---|

| ZET Credit Card | ₹2,000 |

| SBI Unnati Card | ₹25,000 |

| Kotak 811 #DreamDifferent | ₹5,000 |

| ICICI Instant Platinum | ₹10,000 |

| Axis Insta Easy | ₹10,000 |

ZET’s ₹2,000 entry point is significantly more accessible than most bank-issued secured cards. For students and young professionals just starting out, this removes a major barrier that competing products maintain.

The credit limit is directly linked to your FD amount. To increase your credit limit, increase your FD. For credit score building purposes, a ₹5,000–₹10,000 FD with regular usage and consistent payment is enough to generate meaningful credit bureau reporting.

Interest on FD: Does Your Money Still Grow?

Yes — and this is one of ZET’s most important features that distinguishes it from prepaid cards or wallet-based credit products.

Your FD earns interest at up to 7% per annum (subject to change — verify current rate in the app before signing up). This means:

- ₹10,000 FD earns approximately ₹700 per year at 7%

- ₹25,000 FD earns approximately ₹1,750 per year

- ₹50,000 FD earns approximately ₹3,500 per year

The FD interest is credited to your account as per standard FD terms. Your principal is not touched as long as you pay your credit card bills on time. The FD is held as collateral — not consumed.

This is fundamentally different from a prepaid card where you load money and it sits earning nothing. With ZET, your security deposit works for you.

Important: Interest rates on FDs are subject to regulatory changes and partner bank policies. Always verify the current rate directly in the ZET app before making your FD.

Fees and Charges: What Does ZET Actually Cost?

Transparency on fees is critical for any honest ZET App review. Here’s the complete picture:

| Fee Type | Amount |

|---|---|

| Joining Fee | ₹0 |

| Annual Fee | ₹0 (Lifetime Free) |

| FD Minimum | ₹2,000 |

| Late Payment Fee | Standard credit card late fees apply |

| Cash Advance Fee | Applicable if cash is withdrawn |

| Foreign Transaction Fee | Check current rates in app |

| Card Replacement Fee | Verify in app |

The card is lifetime free on the annual fee front — there is no year-on-year charge for holding the card. However, standard credit card charges apply for late payments, cash advances, and any other transactions that carry fees under the card’s terms and conditions.

Always read the complete Terms and Conditions in the ZET app before creating your FD and activating your card.

ZET Credit Score: How Does It Actually Build Your Score?

This is the most important functional question in any ZET App review because it’s the core reason people download the app.

ZET reports your credit card usage to CIBIL (TransUnion) and Experian — two of India’s four major credit bureaus. The reporting covers:

- Credit utilisation (how much of your limit you’re using)

- Payment history (paid on time or late)

- Account age (how long the credit card has been active)

- Account status (active, closed, delinquent)

For someone with zero credit history, just having an active credit card being reported is a significant positive. Credit bureaus need data to generate a score — ZET provides that data through consistent monthly reporting.

The timeline most users experience:

- Month 1–2: Account opens, initial reporting begins

- Month 3–4: First CIBIL score typically appears (NTC — New To Credit)

- Month 6: Score stabilises based on payment behaviour

- Month 9–12: Score of 700+ is achievable with perfect payment history and controlled utilisation

Critical tips for maximum credit score building on ZET:

Keep credit utilisation below 30% of your limit. If your credit limit is ₹5,000, try not to use more than ₹1,500 in any given month. High utilisation signals credit stress and reduces your score.

Pay the full statement amount — not just the minimum due. Minimum payments keep you in good standing but don’t demonstrate the same repayment quality as full payment.

Who Should Use ZET?

ZET is the right product for a specific profile of user. Here’s who will get the most value:

First-time credit card applicants who’ve been rejected If you’ve applied for a credit card at HDFC, Axis, or any major bank and been told your credit score is too low or you have no credit history, ZET gives you an alternative entry point.

Students aged 18–25 building financial foundation College students and recent graduates entering the job market with zero credit history. ZET is accessible on a student budget with a ₹2,000 minimum FD.

Gig workers, freelancers, and self-employed individuals Traditional credit cards require salary slips and ITR. ZET’s FD model bypasses income verification entirely — if you have ₹2,000 to deposit, you qualify.

Salaried individuals with thin credit files Someone who has been employed for 1–2 years, pays all bills on time, but simply hasn’t had a credit product yet. ZET bridges the gap between financial responsibility and credit bureau recognition.

People rebuilding after financial setbacks If your credit score has dropped due to past issues and mainstream banks won’t approve you, ZET provides a clean slate to rebuild.

Who Should Avoid ZET?

Being honest about who ZET isn’t right for is as important as promoting its benefits.

People who already have a good credit score (700+) If your CIBIL score is already above 700, you qualify for better unsecured credit cards with higher limits, cashback, and rewards. ZET adds no unique value for you.

Users looking for rewards, cashback, or travel points ZET’s card is a credit-building instrument, not a rewards product. If your priority is earning cashback on groceries or lounge access at airports, look elsewhere.

Users who need high credit limits immediately Your ZET credit limit equals your FD amount. If you need a ₹1 lakh credit limit, you need ₹1 lakh in FD — which is better deployed in a regular FD with a mainstream bank card.

People who struggle with credit card discipline The credit-building benefit only works if you pay on time every month. If you have a history of missed payments or tend to overspend, a credit card — any credit card — will hurt more than help.

My Personal Experience Using ZET

I want to be straightforward here: I downloaded and used the ZET app primarily to understand whether it delivers on the credit-building promise for a real user — not just on paper.

The onboarding was genuinely fast. I had the app downloaded, KYC completed, FD created, and virtual card activated in under 15 minutes. That’s not a marketing claim — that was my actual experience. No branch visit, no physical document submission, no callback from an agent.

What I particularly appreciated was the transparency of the process. Every step in the app told me exactly what was happening — FD amount confirmed, credit limit set, card number and CVV available for immediate online use. There was no ambiguity about what my money was doing.

I used the card for small monthly expenses — a streaming subscription and a utility bill — and paid the full statement amount on time each month. Within four months, my credit bureau report showed the ZET account actively contributing to my score.

The experience wasn’t perfect. The credit limit tied to FD amount is a real constraint — if you start with ₹2,000, you have ₹2,000 of credit limit, which limits what you can use the card for meaningfully. I’d recommend starting with at least ₹5,000–₹10,000 FD to make the card practically useful for regular monthly spending while keeping utilisation healthy.

Customer care response was adequate — not exceptional. For straightforward queries, the in-app support worked. For more complex issues, response times could be improved.

Overall: ZET does what it promises. If the goal is to build credit history from scratch with a minimal financial commitment, it delivers.

ZET Pros and Cons

| Pros | Cons |

|---|---|

| Lifetime free credit card | Low credit limit tied to FD amount |

| ₹2,000 minimum FD — very accessible | No cashback or rewards on spending |

| FD earns interest up to 7% p.a. | Limited to credit-building use case |

| Reports to CIBIL and Experian | Customer support could be faster |

| No income proof required | FD locked during card tenure |

| Instant digital activation | Not suitable for users with good credit |

| Credit score tracking in app | Interest rates subject to change |

| Suitable for all employment types | Physical card delivery takes time |

Is ZET Safe?

Yes — ZET is a safe fintech platform for its stated purpose. Here’s why:

Your FD is your money. ZET does not consume your deposit. It sits as a Fixed Deposit earning interest. The credit card is issued against it as collateral — not as a loan you’re taking against the company’s money.

Credit bureau reporting is legitimate. Reporting to CIBIL and Experian requires formal bureau membership and compliance with bureau reporting standards. ZET’s reporting is real and verifiable — you can check your CIBIL report independently after a few months to confirm.

Data security. The app handles KYC data and financial information. Standard data protection practices apply — always use the official app from the Play Store or App Store and never share your OTP or PIN with anyone.

Regulated partner banks. The underlying FD and credit card products are issued through regulated banking and NBFC partners under RBI oversight.

Is ZET RBI Approved?

This is one of the most searched questions in any ZET App review and deserves a clear, honest answer.

ZET operates as a fintech platform that works with RBI-regulated banking and NBFC partners for the underlying financial products (FD and credit card). The FD and credit card are issued by these regulated partner entities – not by ZET directly as a bank.

This is a standard and legitimate structure in Indian fintech. Platforms like Fi, Jupiter, Niyo, Slice, and OneCard all operate on similar partnership models — the fintech provides the technology and user experience, while a licensed bank or NBFC provides the regulated financial product.

What this means for you:

- Your FD is held with an RBI-regulated entity

- The credit card is issued under RBI-regulated card issuance norms

- ZET itself is a technology platform operating in compliance with applicable regulations

Recommendation: Verify the current partner bank or NBFC details directly in the ZET app. The regulated entity behind your FD and card should be clearly disclosed in the app’s terms and conditions.

For authoritative information on RBI-approved banks and NBFCs, refer to the official RBI website: https://www.rbi.org.in

ZET Credit Card Customer Care Number

For customer support, ZET provides in-app support as the primary contact channel.

How to reach ZET customer care:

- In-app support: Open the ZET app → Help/Support section → Raise a ticket or start a chat

- Email support: Check the official ZET app for the current support email address

- Official website: https://zetapp.in

Important: Customer care contact details change periodically. Always use the support contact information available within the official ZET app rather than third-party websites that may have outdated information.

Do not share your OTP, PIN, card number, or CVV with anyone claiming to be ZET customer care — legitimate support agents will never ask for this information.

ZET Credit Card Login

Logging into your ZET account is done entirely through the ZET mobile app — there is no separate web login portal at the time of writing.

ZET Credit Card Login process:

- Open the ZET app on your smartphone

- Enter your registered mobile number

- Verify via OTP sent to your mobile

- Access your dashboard — card details, FD status, credit score, transaction history

The app uses OTP-based authentication — there is no static password, which is a security feature. Your account can only be accessed from your registered mobile number.

Alternatives to ZET: How Does It Compare?

If you’re evaluating ZET, it’s worth knowing how it compares to alternatives in the secured credit card and credit-building space in India:

| Feature | ZET | SBI Unnati | Kotak 811 | IDFC FIRST WOW |

|---|---|---|---|---|

| Minimum FD | ₹2,000 | ₹25,000 | ₹5,000 | ₹10,000 |

| Annual Fee | Lifetime Free | Free (4 yrs) | ₹500 | ₹0 |

| FD Interest | Up to 7% | Standard SBI rate | Kotak rate | IDFC rate |

| Income Proof | Not required | Not required | Not required | Not required |

| Credit Reporting | CIBIL + Experian | CIBIL | CIBIL | CIBIL |

| App Experience | Modern, digital-first | Traditional banking | Moderate | Moderate |

| Credit Limit | 100% of FD | Up to FD amount | Up to FD | Up to FD |

ZET’s primary competitive advantages are the lowest minimum FD (₹2,000), modern app experience, and dual bureau reporting (CIBIL + Experian). For users who want the most accessible entry point into secured credit cards, ZET leads on accessibility.

For users who prefer the security of a major public sector bank, SBI Unnati is a strong alternative despite the higher FD requirement.

Final Verdict: Is ZET Worth It in 2026?

After a thorough ZET App review — testing the product personally, studying the fee structure, understanding the credit-building mechanism, and comparing it against alternatives — the verdict is clear:

ZET is the right product for a specific, underserved group of Indian consumers: people who want to build or rebuild their credit score but have been locked out of mainstream credit products.

For this audience, ZET delivers genuine, tangible value:

- The ₹2,000 minimum FD makes it accessible to almost anyone

- Your money earns interest while powering your credit card

- Lifetime free card eliminates the cost barrier

- CIBIL and Experian reporting creates real, verifiable credit history

- Instant digital onboarding removes the friction of traditional bank processes

It is not a rewards card. It is not a high-limit card. It is not for people who already have good credit. It is a credit-building instrument — and as a credit-building instrument, it does its job well.

If your goal is to build a credit score, unlock future financial products, and start your credit journey with minimal risk and minimal commitment — ZET deserves to be at the top of your list.

Ready to start building your credit score?

If you’ve decided to try ZET after reading this review, you can download the app using my referral link below. It supports this website at no extra cost to you.

Disclaimer: This article is based on personal experience and publicly available information. Fees, interest rates, and features are subject to change — always verify current terms directly in the ZET app before signing up. This article contains a referral link. This is not financial advice.

Frequently Asked Questions

What is ZET App? ZET is a fintech app that offers a secured credit card backed by a Fixed Deposit (FD). It is designed to help people with no credit history build a CIBIL score through responsible credit card usage. The minimum FD required is ₹2,000.

Is ZET RBI approved? ZET operates through RBI-regulated banking and NBFC partners who issue the underlying FD and credit card. The financial products are regulated — verify the current partner bank details in the app’s terms and conditions.

What is the minimum FD amount for ZET Credit Card? The minimum FD required to get the ZET Credit Card is ₹2,000 — one of the lowest minimums among secured credit card products in India.

Can ZET really improve my credit score? Yes. ZET reports your credit card usage and payment behaviour to CIBIL and Experian every month. Consistent on-time payments and controlled credit utilisation build a positive credit history. Most users see their first CIBIL score within 3–6 months.

Does my money earn interest in ZET? Yes. Your FD earns interest at up to 7% per annum (subject to change — verify current rate in app). Your principal is not consumed — it remains yours throughout the tenure.

Is ZET credit card free? The ZET Credit Card is lifetime free — no joining fee and no annual fee. Standard credit card charges apply for late payments, cash advances, and other specific transactions.

What is the ZET Credit Card customer care number? ZET’s primary support channel is in-app support. Access it via Help/Support within the ZET app. Always use the contact details provided in the official app.

How do I login to my ZET Credit Card account? Log in through the ZET mobile app using your registered mobile number and OTP verification. There is no separate web portal.

Who should use ZET? ZET is ideal for first-time credit card applicants, students, gig workers, freelancers, and anyone with no credit history who wants to build a CIBIL score with minimal financial commitment.

Is ZET safe to use? Yes. Your FD is your own money held with a regulated partner entity. ZET does not consume your deposit. Standard data security practices apply — use only the official app and never share OTP or PIN.

External Resources:

- RBI official website: https://www.rbi.org.in

- CIBIL official score check: https://www.cibil.com

- Experian India: https://www.experian.in

- NPCI official site: https://www.npci.org.in

- ZET official website: https://zetapp.in