Wint Wealth vs Stable Money is the comparison every serious Indian fixed-income investor is running right now. And it makes complete sense — both platforms are SEBI-registered, both promise returns above FDs, and both have been downloaded by lakhs of users in a relatively short time.

On the surface, they seem interchangeable. But once you go beyond the marketing and look at how each platform is actually built, how they select bonds, how they protect your money, and what they’re ultimately optimized for — the differences are stark.

I’ve studied both platforms in detail. This article breaks down Wint Wealth vs Stable Money across every dimension that actually matters to an investor: returns, bond quality, platform philosophy, safety mechanisms, fees, liquidity, and real-world usability.

By the end, you’ll know exactly which one deserves your capital — and why.

Why the Wint Wealth vs Stable Money Question Is Being Asked More in 2026

The Wint Wealth vs Stable Money debate has picked up serious momentum for a very specific reason: Indian retail investors are finally waking up to the corporate bond market.

For decades, the average investor’s playbook looked like this — park safe money in bank FDs at 6–7.5%, and take equity risk with the rest.

The middle ground — high-quality corporate bonds offering 9–12% fixed returns — was almost entirely inaccessible to retail investors.

Minimum investment sizes were large, documentation was complex, and there was no clean digital interface to discover and buy bonds.

That wall has now been broken. Platforms like Wint Wealth and Stable Money have brought bond investing to retail investors — and suddenly, a whole category of comparison has emerged.

Which platform has better bonds? Which one is safer? Which one gives you more for your money?

The Wint Wealth vs Stable Money comparison is essentially asking: now that we can access bonds, which door should we walk through?

What Is Wint Wealth? A Deep Dive

Wint Wealth is a SEBI-registered Online Bond Platform Provider (OBPP) with registration number INZ000313632, headquartered in JP Nagar, Bengaluru.

It was originally founded in 2020 under the name GrowFix and rebranded to Wint Wealth following backing from prominent fintech investors connected to Zerodha, CRED, Groww, and Dhan.

The platform is laser-focused on one product: senior secured corporate bonds. That’s not a limitation — it’s a deliberate design choice that has serious implications for the quality of what gets listed.

The Philosophy Behind Wint Wealth

When you understand the founding thesis of Wint Wealth, everything else makes sense. The founders saw a specific problem: retail investors in India had no reliable, transparent, and low-cost way to access corporate bonds.

Every existing channel either required large ticket sizes, charged heavy brokerage, or didn’t offer the kind of collateral-backed bond structures that actually protect investors.

Wint Wealth was built to fix all three problems at once — accessible entry points, zero brokerage, and a strong bias toward senior secured and covered bond structures.

Key Platform Numbers

- Returns: 9–12% fixed p.a.

- Minimum investment: Starting from ₹1,000 (varies by bond)

- Zero brokerage — saves 0.25% vs traditional brokers

- Zero defaults till date across all listed bonds

- ₹3,000+ crores repaid on time

- 22 lakh+ users

- App ratings: 4.5 on Google Play, 4.7 on App Store

- SEBI OBPP License: Granted July 25, 2023

The 2% Co-Investment Policy — The Feature Most Reviews Miss

Here is what separates Wint Wealth from virtually every other bond platform in India, and it’s something that almost no comparison article gives enough weight to: Wint Wealth invests a minimum of 2% of its own capital in every bond it lists on the platform.

Read that again. The platform puts its own money on the line alongside yours.

This is not a marketing claim — it’s a structural mechanism that changes the incentive entirely. In a standard marketplace model, the platform earns listing fees or commissions whether or not the bond performs. Their financial outcome is disconnected from yours.

With Wint Wealth’s co-investment policy, if a bond defaults, Wint Wealth loses money too. That single fact raises the quality bar for every single listing.

It’s the oldest principle in finance: skin in the game. And Wint Wealth has built it into the architecture of how the platform works.

How Wint Wealth Selects and Structures Bonds

The two primary bond structures on Wint Wealth are Senior Secured Bonds and Covered Bonds.

Senior Secured Bonds are backed by specific collateral — in a default scenario, bondholders have a priority claim over the issuer’s assets before equity shareholders or unsecured creditors. This is a fundamentally different risk profile from generic corporate bonds where you’re simply an unsecured creditor.

Covered Bonds take this further by maintaining a dynamic collateral pool. Even if the issuer runs into trouble, payments to bondholders continue from the secured assets in the pool. This structure is widely used in European debt markets and is considered one of the more sophisticated investor protection mechanisms in fixed income.

Most retail bond platforms in India list whatever is available in the market. Wint Wealth specifically hunts for bonds with these structural protections — and then co-invests. The combination is what has produced a zero-default track record across all listed bonds.

➡️ Start investing in bonds with zero brokerage — use Wint Wealth referral code B6B59B: Click here to join Wint Wealth →

What Is Stable Money? Understanding the Platform

Stable Money, built by Stable Alpha Technologies Private Limited (Bengaluru), is a broader fixed-income fintech platform.

It has amassed over 30 lakh users — a larger total user base than Wint Wealth — and offers a noticeably wider product range: fixed deposits from 200+ banks and NBFCs, bonds (via Stable Broking Private Limited operating at stablebonds.in), gold and silver mutual funds, and FD-backed credit cards.

The platform is genuinely well-built for what it is optimized to do. If you want to compare FD rates across 200+ institutions in one app and book in under 3 minutes, Stable Money delivers that experience cleanly.

The FD comparison feature is a real time-saver — instead of visiting 10 different bank websites, you see all rates in one place, filter by tenure, and invest directly.

Stable Money’s bonds are listed through Stable Broking, which holds a SEBI Stock Broker registration and OBPP license — so the regulatory foundation is solid. The bond KYC was also reportedly improved in early 2026 to make onboarding faster.

What Stable Money Does Particularly Well

- FD aggregation: 200+ banks and NBFCs including Suryoday Bank, IndusInd Bank, Shriram Finance, Unity Bank

- DICGC insurance on bank FDs up to ₹5 lakhs — a meaningful safety net for conservative investors

- Diversified product range in one app (FDs + bonds + gold/silver MFs + credit card)

- Simple, intuitive UI that has earned it 30 lakh+ users

But here is the honest assessment: Stable Money is an FD platform that also offers bonds. Wint Wealth is a bonds platform, full stop.

That distinction matters enormously when you’re specifically evaluating where to put your bond money.

In the Wint Wealth vs Stable Money conversation, this is the core asymmetry. One platform treats bonds as its entire identity. The other treats them as one item on a larger menu.

Wint Wealth vs Stable Money: Full Head-to-Head Comparison

| Feature | Wint Wealth | Stable Money |

|---|---|---|

| Primary Product | Bonds (specialist) | FDs (bonds secondary) |

| Bond Returns | 9–12% p.a. | Up to 12% p.a. |

| Min. Bond Investment | From ₹1,000 | Varies by bond |

| Brokerage on Bonds | Zero | Not explicitly zero |

| Platform Co-invests | Yes — min 2% per bond | No |

| Zero Default Record | Yes — all listed bonds | Not publicly stated |

| FD Products | No | 200+ banks/NBFCs |

| DICGC Insurance | Not applicable | Yes, on bank FDs |

| Bond Structure Focus | Senior Secured + Covered | Handpicked, less public detail |

| Backed By | Zerodha/CRED/Groww/Dhan investors | Institutional funding |

| SEBI OBPP License | Yes — INZ000313632 | Yes — Stable Broking |

| Sell Before Maturity | Yes — sell anytime feature | Subject to bond terms |

| App Rating | 4.5 / 4.7 | 4.5+ |

| Users | 22 lakh+ | 30 lakh+ |

Wint Wealth vs Stable Money: The 5 Deciding Factors

When investors search Wint Wealth vs Stable Money, they’re really asking about five things. Let’s go through each one with the depth it deserves.

1. Bond Quality and Curation

This is where Wint Wealth vs Stable Money diverges most sharply, and it’s the factor that matters most.

Wint Wealth’s entire business model, reputation, and track record rests on bond quality. They have a dedicated due diligence process, a preference for specific bond structures (senior secured, covered bonds), and — most crucially — a co-investment policy that ties their financial outcome to yours. They cannot afford to list a bad bond. Their business lives and dies by the quality of what they put on the platform.

Stable Money lists “handpicked, vetted bonds” — but the public detail on their curation methodology, collateral structures, and due diligence process is considerably thinner. For an investor trying to make an informed decision in the Wint Wealth vs Stable Money comparison, that information gap matters.

Winner: Wint Wealth, and it’s not close.

2. Effective Returns After All Costs

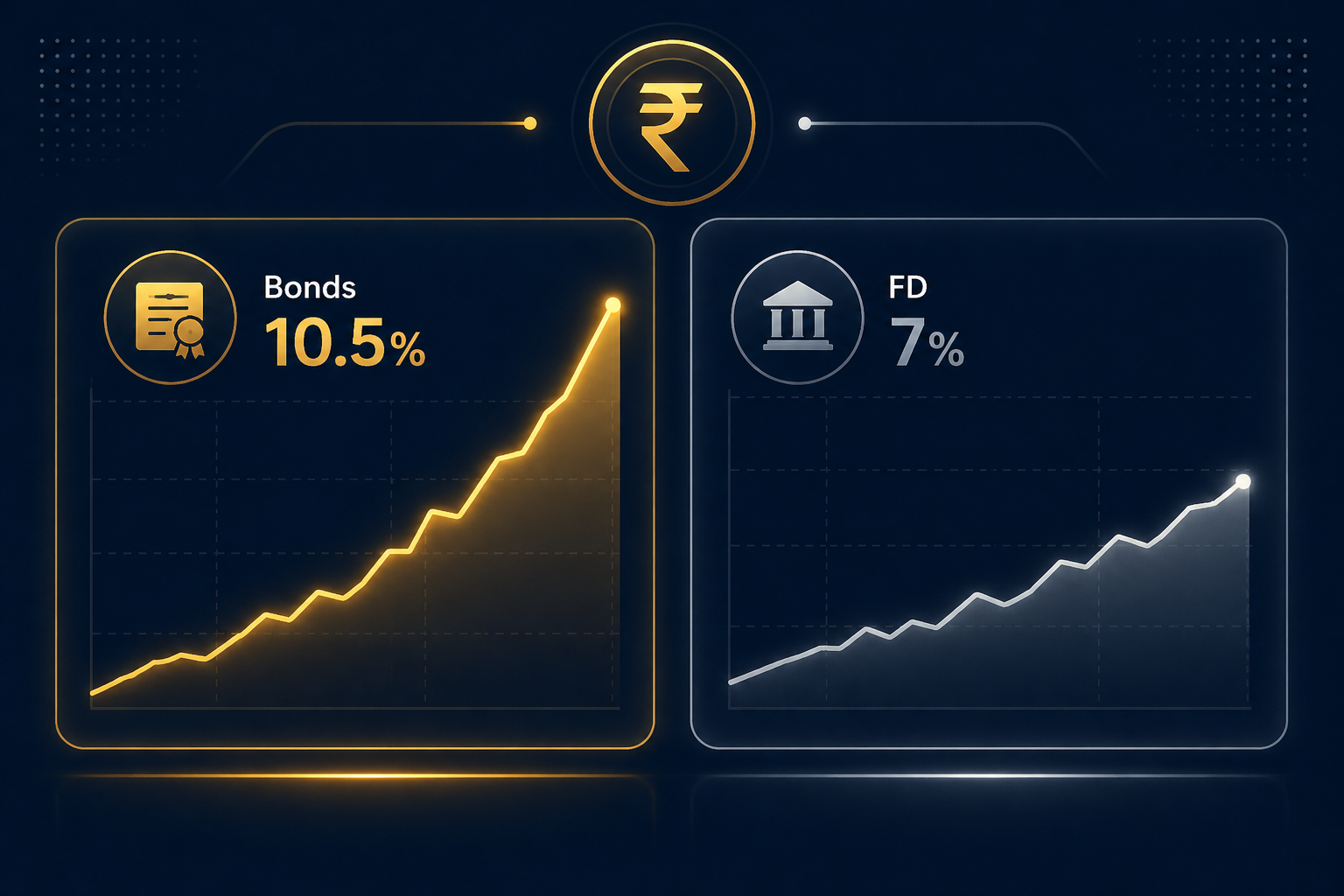

Both platforms advertise bond returns in the 9–12% range. At the headline level in the Wint Wealth vs Stable Money comparison, returns appear similar. But the actual return you get in your account depends on more than the coupon rate.

Wint Wealth’s zero brokerage policy means your effective return is higher for an equivalent bond. If a bond yields 10.5% and another platform charges 0.25% brokerage, your net yield is 10.25%. On Wint Wealth, it’s the full 10.5%. On ₹5 lakhs, that 0.25% difference is ₹1,250 per year — and over a 3-year tenure, that’s ₹3,750 in your pocket just from zero brokerage.

Winner: Wint Wealth (on effective, net-of-cost returns).

3. Safety Architecture

Both platforms are SEBI-regulated — that’s the non-negotiable baseline. But safety in bond investing goes far deeper than a regulatory badge, which is exactly what this Wint Wealth vs Stable Money analysis is designed to surface.

Wint Wealth’s zero-default record across all bonds listed since inception is the most concrete safety signal available. Add the co-investment policy, the senior secured and covered bond structures, and the institutional backing, and you have a multi-layered safety architecture that goes well beyond compliance.

Stable Money’s safety story is genuinely strong for FDs (DICGC insurance up to ₹5 lakhs) but far less publicly detailed for the bond side.

Winner: Wint Wealth for bonds. Stable Money for FD safety.

4. Product Breadth

This is the one area in the Wint Wealth vs Stable Money comparison where Stable Money genuinely wins. If you want FDs, bonds, gold mutual funds, and a credit card under one login, Stable Money provides that one-stop experience. Wint Wealth doesn’t offer FDs or gold products — it deliberately stays in its lane.

For investors who want to consolidate everything in one app, Stable Money has more options.

Winner: Stable Money (on breadth).

5. Platform Credibility and Track Record

Wint Wealth’s backers include investors from Zerodha, CRED, Groww, and Dhan — arguably the four most credible and execution-proven names in Indian retail fintech. These aren’t passive cheque writers; they’re operators who have built large financial platforms in India and understand exactly how this market works. The fact that they evaluated Wint Wealth and backed it is a meaningful signal.

In the Wint Wealth vs Stable Money credibility comparison, both platforms are legitimate, but Wint Wealth’s investor roster and the depth of its publicly documented track record give it a clear edge.

Winner: Wint Wealth.

Real Numbers: What ₹1 Lakh Looks Like After 3 Years

Let’s make this concrete with actual return projections from the Wint Wealth vs Stable Money analysis.

Scenario: ₹1,00,000 invested for 3 years

| Investment Option | Annual Rate | Approximate Value at Maturity |

|---|---|---|

| SBI Bank FD | ~6.8% p.a. | ~₹1,21,900 |

| Small Finance Bank FD | ~8.5% p.a. | ~₹1,27,700 |

| Wint Wealth Bond (conservative) | 9.5% p.a. | ~₹1,31,400 |

| Wint Wealth Bond (typical) | 10.5% p.a. | ~₹1,34,900 |

| Wint Wealth Bond (high yield) | 12% p.a. | ~₹1,40,500 |

On a ₹1 lakh investment, the gap between a standard bank FD and a typical Wint Wealth bond is roughly ₹13,000–₹18,000 over 3 years. Scale to ₹10 lakhs and that’s ₹1.3–₹1.8 lakhs of additional wealth on the same principal, same tenure, same tax bracket.

That gap is simply too large to ignore — and it’s why the Wint Wealth vs Stable Money question has become so financially important for serious investors.

The Liquidity Reality: What Neither Platform Says Loudly Enough

When comparing Wint Wealth vs Stable Money on bonds, one thing both platforms tend to underemphasise is liquidity — and investors need to understand this clearly before committing.

Unlike a bank FD where you can break it prematurely (with a small penalty), corporate bond liquidity depends on secondary market conditions. Wint Wealth offers a “sell anytime” feature, which is genuinely better than most platforms — but secondary market depth for Indian corporate bonds remains limited. If you need to exit urgently, you may receive a price below face value.

This is not a specific flaw of either platform in the Wint Wealth vs Stable Money comparison — it’s an Indian bond market infrastructure reality. The practical advice: invest in bonds only with money you can comfortably hold till maturity. Treat them like a 2–3 year commitment, not a liquid instrument.

Who Should Choose Wint Wealth?

After a thorough Wint Wealth vs Stable Money analysis, Wint Wealth is the right choice if:

- You want bonds as your primary fixed-income instrument

- You’re looking to earn 9–12% with structured collateral security

- You value the platform co-investing alongside you (skin in the game)

- You want to maximize net returns through zero brokerage

- You’re comfortable with a 2–3 year hold-to-maturity horizon

- You’ve maxed out FDs and are looking for higher-yield alternatives

- You’re building a serious fixed-income portfolio

➡️ Sign up on Wint Wealth using referral code B6B59B — zero brokerage, zero defaults till date, 9–12% fixed returns: Join Wint Wealth here →

Who Should Choose Stable Money?

In the Wint Wealth vs Stable Money comparison, Stable Money makes more sense for:

- Investors whose primary focus is FD comparison and booking across multiple banks

- Conservative investors who prioritize DICGC-insured deposits above all else

- Those who want FDs, bonds, gold mutual funds, and a credit card in one single app

- Investors just beginning their fixed-income journey and want a broader starting point

The Final Verdict: Wint Wealth vs Stable Money

The Wint Wealth vs Stable Money debate has a clear answer once you define the use case.

For bond investing specifically, Wint Wealth wins decisively — on bond quality, platform philosophy, co-investment policy, zero brokerage, zero-default record, institutional credibility, and structural bond protections. There is no meaningful category in the Wint Wealth vs Stable Money analysis where Stable Money beats Wint Wealth when the focus is bonds.

For FD investing, Stable Money wins — its 200+ bank aggregation is unmatched and the DICGC insurance layer adds genuine protection.

The bottom line in the Wint Wealth vs Stable Money question: if you’re here because you want to invest in bonds, use Wint Wealth.

If you primarily want FDs with bonds as an occasional supplement, Stable Money works for that. But for serious fixed-income investors systematically building wealth at 9–12%, the Wint Wealth vs Stable Money answer is unambiguous.

➡️ Get started with Wint Wealth today — use referral code B6B59B for zero brokerage on your first bond investment: Start Investing on Wint Wealth →

Conclusion

Every few years, a new financial instrument becomes accessible to Indian retail investors at scale — and corporate bonds are having that moment right now. The Wint Wealth vs Stable Money question is the first major fork in the road in this new landscape.

Wint Wealth has built the better bond platform. Their co-investment model, senior secured bond structures, zero brokerage, zero-default track record, and backing from India’s most credible fintech investors make them the most trustworthy option for bond-first investors. In the Wint Wealth vs Stable Money debate, no amount of FD aggregation or product diversification changes that conclusion when bonds are the goal.

Stable Money is a good product — particularly for FD discovery and booking. But a generalist can never match a specialist when the specialist has gone this deep into one domain.

For bonds, the answer in the Wint Wealth vs Stable Money question is clear: go with Wint Wealth.

➡️ Sign up now using Wint Wealth referral code B6B59B — 9–12% fixed returns, zero brokerage, zero defaults till date: https://www.wintwealth.com/bonds/referral/invite?referralCode=B6B59B

FAQs: Wint Wealth vs Stable Money

Q1. Which is better for bonds — Wint Wealth or Stable Money? In the Wint Wealth vs Stable Money comparison, Wint Wealth is clearly better for bond investing. It has a deeper curation process, a co-investment policy, senior secured bond structures, zero brokerage, and a zero-default track record since inception.

Q2. What is the Wint Wealth referral code? The Wint Wealth referral code is B6B59B. Use it at signup to invest with zero brokerage benefits. Sign up here →

Q3. Is Stable Money safe for investing? Yes, Stable Money is a SEBI-registered and RBI-compliant platform. It’s particularly reliable for FD investments where DICGC insurance covers up to ₹5 lakhs. For bonds, it’s legitimate but less specialized than Wint Wealth.

Q4. Does Wint Wealth charge any brokerage? No. Wint Wealth charges zero brokerage on all bond investments, saving approximately 0.25% vs traditional brokers — meaningful savings at scale.

Q5. What returns does Wint Wealth offer? Wint Wealth bonds offer 9–12% fixed returns per annum depending on the specific bond, issuer credit rating, tenure, and payout frequency.

Q6. Has any bond on Wint Wealth ever defaulted? As of the time of writing, Wint Wealth has maintained a zero-default record across all bonds listed on its platform. Note: this is not a guarantee of future performance and all bond investments carry inherent credit risk.

Q7. What is the minimum investment on Wint Wealth? You can start investing on Wint Wealth from as low as ₹1,000, though individual bonds may have higher minimums depending on the issuance structure.

Q8. Which is better for FDs — Wint Wealth or Stable Money? For FDs, Stable Money is the better choice. It aggregates 200+ banks and NBFCs, offers DICGC insurance, and makes FD comparison and booking seamless. Wint Wealth focuses exclusively on bonds.

Q9. Can I withdraw bond investments early on Wint Wealth? Wint Wealth has a “sell anytime” feature, but secondary market liquidity for Indian corporate bonds is limited. It’s advisable to invest with a hold-to-maturity approach for best results.

Q10. Is Wint Wealth regulated by SEBI? Yes. Wint Wealth (Wint Securities Private Limited) is a SEBI-registered Stock Broker and OBPP with registration number INZ000313632, NSE membership number 90328, and DP registration INDP7592023.

Resources

- SEBI OBPP Regulatory Framework — Understand the licensing structure for bond platforms

- RBI Corporate Bond Market Guidelines — Policy and regulatory context for debt instruments

- NSE Debt Segment Overview — Secondary market infrastructure for corporate bonds